Why didn't anyone point out the flawed operating leverage story in SaaS?

A persistently negative operating margin was there in plain sight

One of the first things I noticed when I started as a VC in 2022 was that the average listed Software as a Service company (SaaS) was making an operating loss.

At the time, I had the intuition that the space was crowded and not where I could generate alpha. But this wasn’t the dominant sentiment. As an Associate, I had to strike a balance between my (potentially wrong) views on where to invest and what had previously driven the fund's success1. They asked me to analyze more SaaS, so I tried to meet them halfway.

My style is to ask, 'What do the best in-class companies in this sector look like?’ As a first step in broadening my knowledge, I’d go to their publicly available financial statements and look at their metrics.

I knew the story with SaaS was that they have operating leverage. But was this true? Operating leverage within software is the alluring idea that once you’ve invested the money to build the product, you’ll have a close to zero marginal cost product to sell. Therefore, as you continue to add customers on a recurring revenue basis, you’ll be spreading the less variable operating costs over more customers. In that case, you should see your operating costs as a % of revenue decline, bringing in increasing net profit dollars. This is why, if you’d had read something about getting into VC a few years back, it was dominated by one piece of advice—learn unit economics.

Yes, unit economics matter for the end state of a company. But the error is that in isolation, they mean little. We cannot ignore the other key elements of what the world’s best businesses use to sustain a competitive advantage. It seemed many were too focused on gross margin (unit economics) and not focused enough on things like barriers to entry. For example, your unit economics are only viable if there are high enough barriers to prevent another competitor from building the same product and undercutting the price, or investing more in marketing. These barriers can be things like switching costs (if you’ve gained market share, is there a disincentive for your customer to switch to another provider), or technical moats like intellectual property or generally hard-to-solve technical problems2.

Without this nuance, it was easy to believe the operating leverage story. What, with 75+% gross margins and more customers to spread your ‘fixed’ operating costs over, you’ll eventually turn into a cash-generating machine!

The thing was, this was a theoretical idea for which there was less evidence in practice. Besides a few major winners—usually more on the infrastructure/database side—I couldn’t see where this story was still coming from. We were well over a decade into the SaaS ‘revolution’, so shouldn’t these companies finally be realizing the operating leverage dream? Why didn’t anyone say anything?

Reality is there for you to see if you simply look and think for yourself

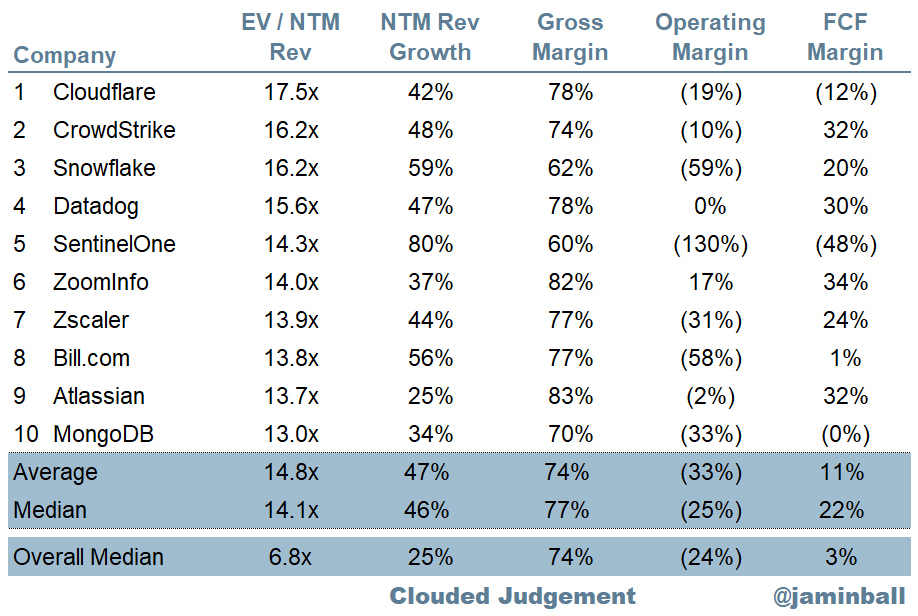

If you looked at the financials, it was clear that even amongst the fastest-growing listed software companies in the world, those considered 'successful', the operating leverage story wasn’t there. Sure, the gross margin appeared high! However, the average operating margin was persistently negative3. Still, when I spoke to other investors about this, they denied it or suggested I was not understanding something.

Now the story has flipped. SaaS is a meme, perhaps overcorrecting in the opposite direction. But point aside, I’m seeing investors left, right, and center write about how SaaS might not be the best business model in the world after all. Now they’re into deep tech, or AI, or whatever other trend they’re jumping on.

Here’s a quote from Benn Stancil’s April 2024 post, ‘Do software companies actually have good margins?’.

And yet! According to Jamin Ball’s figures, the average public software-as-a-service company has gross margins of 74 percent—it only costs them a dollar to manufacture something they can sell for four dollars. This is almost double the gross margin of the average company in the S&P 500, which is around 40 to 45 percent.5 However, the average operating margin for an S&P 500 company is positive 15 percent, compared negative 11 percent for the average SaaS company. Despite their high gross margins, SaaS companies don’t just make less than other public companies; most of them actually lose money.

Ben may have been one of the first to fully elucidate this problem, and I recommend reading the whole piece for a great description of the issue. However, it was when the divergence was already showing up in the market (keep reading, I’ll explain).

Essentially, when the market started to actually show that money-losing companies are not the same as money-making ones, people started saying the operating leverage story was, perhaps, a little flawed. That’s too late to make money in public markets, and much too late for VCs, who are looking to sell to public markets in 7-10 years.

You can make money in investing by noticing divergences between public perception and underlying reality

The physical reality was always there, and there was money to be made. If you understand roughly how markets price equities, you know that long-duration equities—loss-making companies whose expected positive cash flows are further in the future—do badly in rising interest rate environments.

But that also implies the opposite. When rates are falling, long-duration equities should outperform. That is, if they are truly 'long-duration'—if the dollars they’re investing today (instead of recognizing as profit) will actually drive expanded operating margins in the future.

So what actually happened?

The world saw significant inflation in 2022, which led to rising rates and a subsequent stock market crash, naturally led by these long-duration equities. But if the operating leverage story were true, then as markets started to price falling rates again, you'd expect them to outperform the slower-growing but higher cash-flow positive 'safe' stocks.

And yes, that would happen in theory. So why didn't the Emerging Cloud index outperform the NASDAQ in 2024? Well, because the market is not under the same delusion that the average early-stage VC was. It looks at financial statements, sees a flawed operating leverage story, and prices accordingly.

Did we confuse low interest rates with a dream business model?

Pre-covid was a historical anomaly. Rates were incredibly low, even negative in places like Japan. In that case, you are not discounting expected cash flows far in the future, which really pumps valuations! This potentially lent fuel to the belief that SaaS companies were achieving their dream outcome, rather than benefitting from a historically unusual market environment. For those who ignored the macro or believed ‘this time is different’, it was easy to confuse what I think actually drove high valuations (the rates anomaly, which pushes investors to increasingly risky assets in search of yield) with what everyone was saying (the dream business model).

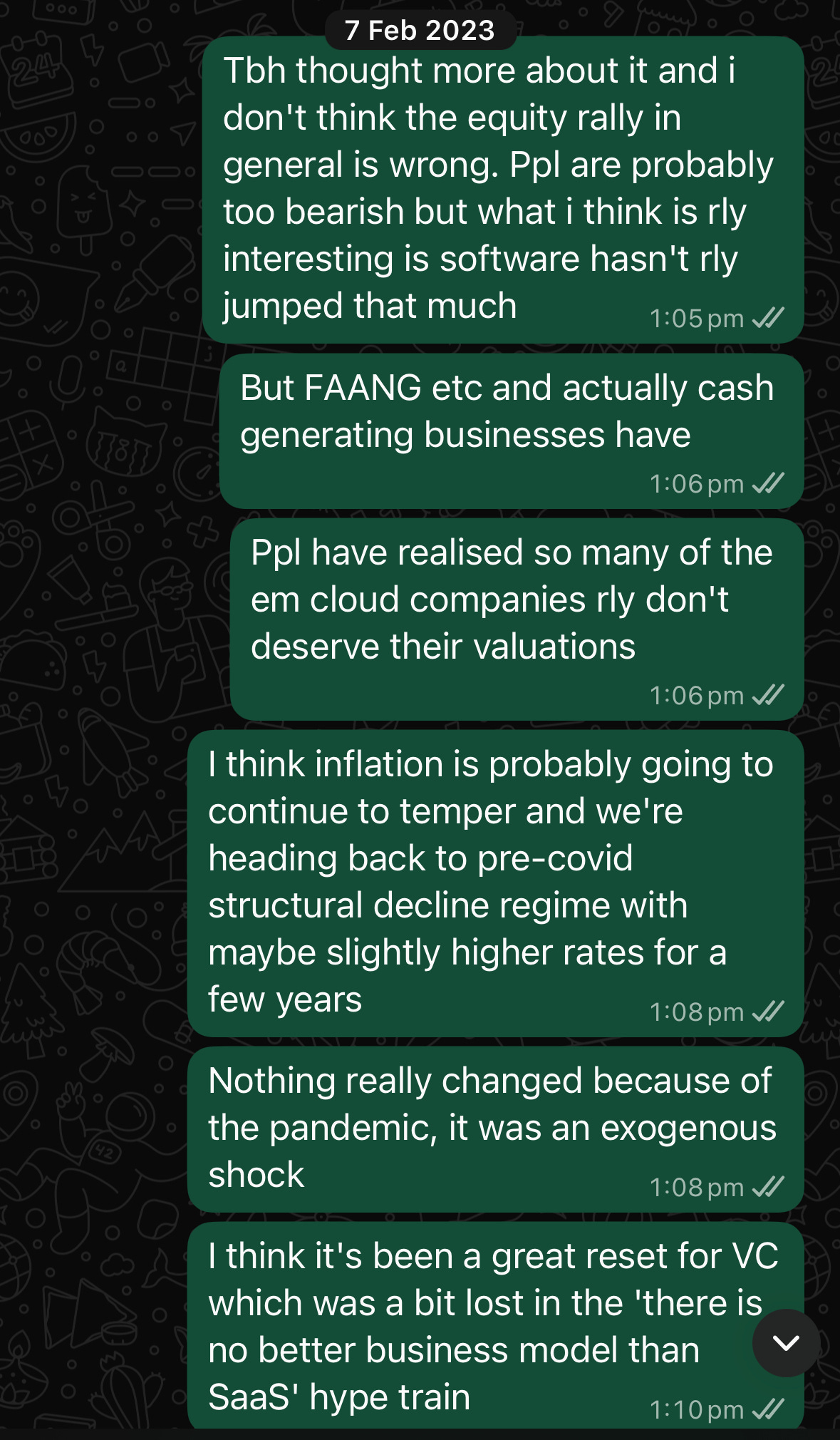

Markets started to rally again in early 2023, which had people confused in a high-inflation environment. I sent one of my managers this message in February of 2023, after which I quickly picked up some bargain, cash-flow generating, or monopoly-like companies with deep moats (e.g., Google & Amazon for <$100).

The whole market was down, big tech included. But this didn't make sense to me. Not all of tech is long-duration. We were in a risk-averse environment now. I thought that when rising rates started to get inflation back under control, and the market started to price falling rates again, people wouldn’t flip back to ultra-risk on. Instead, they’d flock to real cash flow-generating tech and companies with real moats. Essentially, big-tech type stocks would lead.

In 2024, as rates finally started to temper again, we saw exactly this. High gross margin is a mirage if you're having to spend all your operating dollars on improving the product and marketing to maintain market share. You couldn’t hide behind this narrative in a non-zero rate world anymore.

What does this all mean?

Benn’s Substack post mentioned above was from April 2024. It was stating something that, if you look at my chart above, had already happened. My post is also a retrospective, and I want to emphasize two things:

I’m clearly not telling you where the divergences are now

I’m not saying all SaaS businesses are bad, but that they are not automatically the ‘best’ business model

Instead, I’m suggesting we look at financials more holistically and double-check that popular narratives are reflected in reality. This isn’t giving away where you’re going to make money next, but there are certainly more divergences like these4. I’ll try to post about them more in the future. But you should search for them too!

To circle back to my opening question, why did no one trust the numbers right in front of them before the market clearly told us so? You didn’t need to be a macro nerd to see that a negative operating margin over 10 years into a wave doesn’t align with a ‘dream business model’ story.5 Money doesn’t grow on trees, so you’ll eventually need to start generating it.

To be clear, not everyone at this firm disagreed with me. They let me invest in the deep tech company I now work for! I also recognize that, regardless of my personal views, I’d need to opine on SaaS companies in investment committee meetings, so I don’t think the push was wholly unreasonable. It’s simply helpful to illustrate how challenging it is to stand against the crowd, particularly as a junior.

This is a non-exhaustive list, but perhaps we can go into that in another post.

Another can of worms is to look into stock-based compensation (SBC). While many of these companies were growing revenue fast, their free cash flow (FCF) was almost entirely made up of stock-based compensation. For example, in FY 2023, Atlassian posted $842M in FCF—12% growth on the previous year—but they also registered $949M in SBC. Sure, it’s ‘cash’, but it’s diluting shareholders.

Another was the perplexing belief that bio tools companies were where the money would be made in this new ‘tech bio’ wave of 2022. You could see in financial statements that the money was made in drugs/therapeutics. I guess this was somewhat tied to SaaS-mania, though, and projecting those business models onto other industries.

Perhaps VCs could make the argument that they don’t care about stock prices today, because they’ve already exited that wave. The point is that as a VC, you are investing to exit to the stock market in 10 years. You need to be thinking about the future with new investments. In 2022, I didn’t think SaaS would be dominating the IPO market in 2030-2035. And as always, I could be totally wrong from here too. This isn’t financial advice.

Yeah, what I find odd is that you rarely see these businesses treat R&D like capex. They (the R&D employees) just stay on the books, and the spend even grows. I suspect with aggressively declined marginal benefits over time, while maintaining the marginal cost. Or maybe the R&D is a matter of survival (suspicious of this argument), and it truly does represent poor terminal operating margins. I think there is something to the PE shops that buy and cut these kinda companies.

Very interesting. What is the underlying reason(s) for the difference between high gross margin and negative operating margins? Is it mostly the cash-burning customer acquisition arms race kinda dynamic, or something else?